How Mastercard Is Using Stablecoin Infrastructure for Global Payments

Explore how Mastercard is integrating regulated stablecoins into global payments to enable faster, always-on settlement and real-world blockchain adoption.

×

×

Join Our Internship Program

Apply Now →For many years, Mastercard's blockchain strategy has focused primarily on enabling customers to interact with digital assets using familiar payment methods. Through collaborations and pilots, the company explored blockchain applications, facilitated cryptocurrency purchases, and issued branded cards in partnership with cryptocurrency exchanges. Even though these projects showed interest in digital assets, they mostly stayed on the periphery of Mastercard's payment network rather than integrating into its core infrastructure.

Over time, that approach has developed into something far more grandiose. Mastercard is already incorporating regulated stablecoins into several layers of its global payments network, from consumer wallets and merchant settlements to cross-border transfers and, most recently, card settlement itself, rather than viewing blockchain as a distinct ecosystem.

The company's most recent announcement, made on June 3, 2026, is the best proof yet that blockchain is evolving from an experimental service to an integral part of Mastercard's operational infrastructure.

In addition to conventional currency settlement, the new system allows issuers and acquirers to settle qualified card transactions using regulated stablecoins. The program operates across blockchain networks like Ethereum, Base, Arbitrum, Polygon, Solana, Canton, Tempo, and the XRP Ledger (XRPL) and initially supports stablecoins like Circle's USDC, Paxos-issued PYUSD, USDG and USDP, Ripple's RLUSD, and SoFiUSD. It is anticipated that early adopters, such as ARQ (previously DolarApp), CBW Bank, Cross River Bank, Lead Bank, and Nuvei, will start utilising these features throughout the US and Latin America before expanding more widely throughout 2026.

At first glance, this seems like just another payment improvement. In actuality, it signifies a more profound change in the perspective of one of the biggest payment firms in the world about blockchain technology. Instead of supplanting conventional payment rails, Mastercard is introducing blockchain as an additional settlement alternative within the same network. The strategy is part of a larger institutional trend wherein blockchain is being used more and more to enhance particular operational procedures, such as liquidity management, settlement timing, and cross-border efficiency, rather than completely replacing current financial systems.

Most significantly, this announcement was not made in a void. It is the outcome of years of strategic collaborations, acquisitions, and incremental growth that have gradually increased Mastercard's blockchain capabilities. The company's current belief that stablecoins have developed enough to sustain a crucial part of the global payment infrastructure can be better understood in light of this evolution.

- Building an End-to-End Stablecoin Ecosystem, Not Just a Settlement Product

- Why Settlement Has Become Mastercard's Next Blockchain Priority?

- Unlocking Real-World Use Cases: Where Mastercard Sees Stablecoins Creating Value?

- From Consumer Payments to Core Settlement Infrastructure

- What This Means for the Payments Industry & the Broader Blockchain Ecosystem?

- Challenges That Could Influence Mastercard's Stablecoin Strategy

- A Pragmatic Path Forward

Building an End-to-End Stablecoin Ecosystem, Not Just a Settlement Product

The announcement of the settlement in June 2026 is frequently referred to as Mastercard's first stablecoin settlement. But looking at it only in that way ignores the company's larger plan. Instead of launching a single blockchain product, Mastercard has spent the last few years creating a networked ecosystem that allows stablecoins to flow smoothly through all phases of the payment lifecycle, including institutional settlement, merchant acceptance, consumer wallets, and cross-border transfers.

Source: Mastercard

When Mastercard unveiled what it called "end-to-end stablecoin capabilities" in April 2025, this process accelerated dramatically. The business tackled several aspects of the payment ecosystem at once rather than concentrating on just one use case. Wallet providers and financial institutions received infrastructure for transferring stablecoin value throughout Mastercard's network, merchants could opt to receive settlement in regulated stablecoins like USDC, and consumers could spend stablecoins through Mastercard-linked payment cards.

Mastercard took the opposite stance, urging customers to switch from conventional payment systems to blockchain-native settings. Stablecoins emerged as an additional payment alternative within the current financial infrastructure, enabling businesses and consumers to engage with blockchain technology without radically altering how they send and receive money.

Partnerships announced in 2025 helped to further develop the plan. Mastercard partnered with Nuvei and Circle to allow retailers to settle immediately in USDC, regardless of whether customers purchased using digital assets or conventional payment methods. Soon after, the business teamed up with MoonPay to introduce stablecoin-capable credit cards that let consumers use their digital wallet balances at over 150 million retailers that were already linked to Mastercard's worldwide acceptance network.

Mastercard kept funding institutional infrastructure in support of these consumer-facing activities. Through regulatory clearances and acquisitions, the company strengthened its compliance capabilities and increased its support for authorised stablecoin issuers, including Circle, Paxos, Ripple, and subsequently SoFi. Mastercard saw regulatory preparedness as equally crucial as technological innovation, as evidenced by its acquisition of BVNK, a business that specialised in stablecoin payment infrastructure, and its acquisition of a New York BitLicense.

Therefore, the June 2026 settlement announcement is not a stand-alone undertaking but rather the next natural step. Mastercard is expanding blockchain infrastructure into the settlement layer, which links issuers and acquirers, after enabling customers to spend stablecoins, merchants to receive them, wallets to transfer them, and financial institutions to move them across borders. Instead of producing discrete blockchain goods, each stage expands on the capabilities created in earlier years to create a more interconnected ecosystem.

Mastercard's more general approach to blockchain adoption is also reflected in this slow development. The company has continuously concentrated on integrating blockchain, where it can address well-defined operational challenges while maintaining the dependability, security, and compliance standards that financial institutions demand from established payment networks, rather than advocating for the disruptive replacement of current payment systems.

Why Settlement Has Become Mastercard's Next Blockchain Priority?

Most customers rarely consider settlement. A card payment ought to be completed after it is accepted. In actuality, the transfer of funds between banks, card issuers, payment processors, and merchants takes place later through a convoluted settlement procedure that frequently depends on banking hours, a number of middlemen, and payment infrastructure unique to each nation.

Although these methods have long facilitated international trade, they also provide operational difficulties. Because they go via correspondent banking networks, international settlements may take longer. In order to account for delays, weekends, and public holidays, financial institutions frequently need to keep bigger liquidity buffers. These scheduling restrictions can lead to inefficiencies in working capital and treasury management for companies that operate in several marketplaces.

This particular aspect of the payment lifecycle is the focus of Mastercard's most recent endeavour.

As AI agents begin to act, payments move into the background — at machine speed and massive scale.

— Mastercard (@Mastercard) June 10, 2026

Today we’re introducing Mastercard Agent Pay for Machines — bringing structure, governance, and trust to this new class of payments.

Launching with 30+ partners to bring this to… pic.twitter.com/X4zmXIg7FV

Mastercard is using regulated stablecoins as an extra settlement rail that works in combination with conventional fiat infrastructure rather than replacing current settlement systems. The program's issuers and acquirers have the option to settle qualified transactions using stablecoins that are always moving via blockchain networks, even after regular business hours.

This is a crucial distinction. Financial institutions are not being urged by Mastercard to completely switch to digital assets or give up on their current payment systems. While stablecoins only offer an alternative for organisations that can gain from quicker liquidity cycles or round-the-clock settlement, fiat settlement is still an option.

The selection of regulated stablecoins is equally thoughtful. Because they are backed by reserve assets and issued under controlled frameworks, assets like USDC, PYUSD, RLUSD, and USDP are intended to maintain a steady value. Compared to extremely volatile cryptocurrencies, whose exchange-rate swings could bring additional settlement risk, they are far better suited for payment infrastructure due to their rather steady price features.

Additionally, rather than depending on a single blockchain network, the organisation is implementing a multi-chain strategy. The fact that institutional blockchain adoption is growing more multi-network is reflected in support for Ethereum, Base, Polygon, Solana, XRPL, Canton, and other networks. Different blockchains have different advantages, such as reduced transaction costs, increased throughput, regulatory preferences, or specialised enterprise capabilities. Mastercard seems to be planning to stay infrastructure-neutral rather than fully commit to one ecosystem.

Mastercard is successfully bridging the operational divide between blockchain technology and traditional banking by integrating stablecoins into an already-existing payment network rather than creating a whole new one. Instead of becoming a rival financial system, blockchain becomes an additional technological layer facilitating international payments, giving financial institutions more flexibility without having to rethink their payment processes.

Unlocking Real-World Use Cases: Where Mastercard Sees Stablecoins Creating Value?

Settlement is just one part of a much larger plan, even though it has recently been added to Mastercard's blockchain strategy. Over the course of the last two years, Mastercard has repeatedly stressed in its statements that stablecoins shouldn't exist as separate digital assets. Rather, they ought to be programmable money that can be used for business-to-business (B2B) transactions, consumer payments, merchant settlements, cross-border transfers, and treasury activities.

The way Mastercard has constructed its ecosystem demonstrates this concept. The company has concentrated on linking different payment touchpoints so that stablecoins can flow between them without requiring customers to switch between different financial systems, rather than introducing distinct blockchain products for diverse markets.

Breaking news! Mastercard has been granted a BitLicense by the New York State Department of Financial Services (@NYDFS), advancing our commitment to secure and compliant digital asset innovation. 🗽🎉

— Mastercard (@Mastercard) May 27, 2026

Learn more: https://t.co/3aNHu3uwx6

Mastercard Move, the company's international money transfer tool, is among the top examples. Stablecoin transfers will now be supported by Mastercard Move, which has historically been utilised for both domestic and international payouts. This keeps them connected to Mastercard's current payment infrastructure while enabling banks, digital wallets, and licensed financial institutions to send and receive regulated stablecoins internationally. Stablecoins become an additional payment method that can function constantly outside of regular banking hours, rather than taking the place of current remittance channels.

Mastercard One Credential is another significant advancement that allows customers to use a single credential to access a variety of payment options, such as debit, credit, instalments, and digital assets. This product illustrates Mastercard's larger objective of lowering barriers between traditional banking and digital assets, even though it goes beyond blockchain. Stablecoins and fiat money can coexist in the same payment environment, so users do not need to have different payment experiences based on which they are using.

Additionally, Mastercard is increasing the use of stablecoins in merchant payments. Regardless of whether clients paid with traditional payment methods or digital assets, businesses can opt to receive settlement in USDC through agreements with Circle and payment processor Nuvei. This lowers the operational complexity usually associated with Bitcoin payments while providing businesses with more flexibility in managing liquidity.

This concept is further extended to consumer spending through the company's collaboration with MoonPay. Together, the two companies launched Mastercard-branded cards that let customers use their balances in regulated stablecoins at Mastercard's worldwide network of merchants. Customers can spend digital assets using well-known payment methods since the conversion takes place in the background, rather than forcing merchants to accept Bitcoin directly.

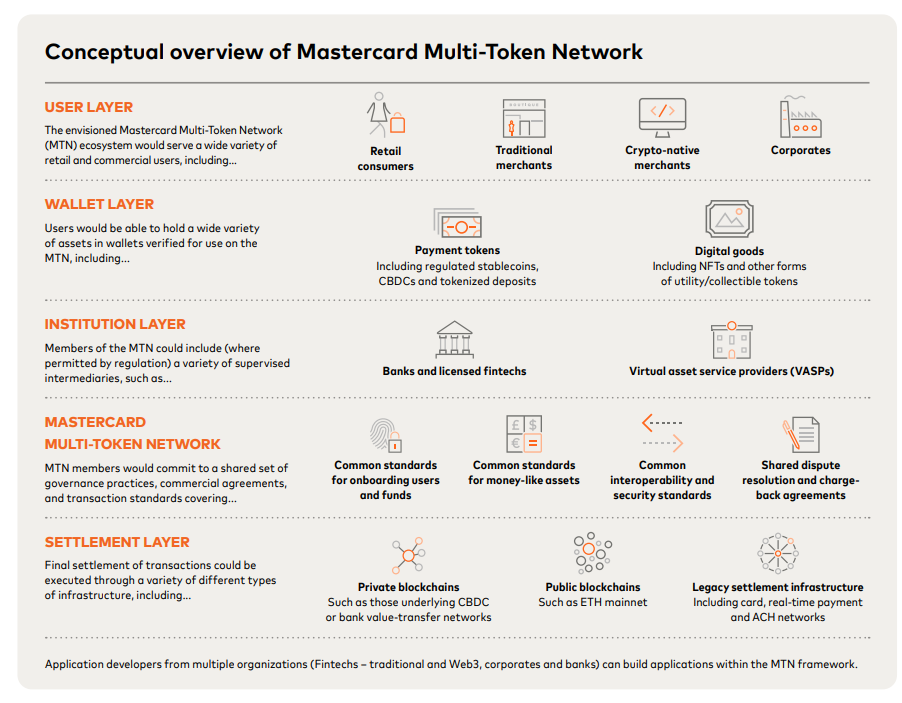

Mastercard's Multi-Token Network (MTN) is arguably the biggest long-term project. MTN is intended for institutional use, as opposed to consumer-facing payment products. It supports programmable payment conditions and gives financial institutions a shared infrastructure for transferring tokenised deposits, stablecoins, and other digital assets.

Source: Mastercard

Practically speaking, this makes it possible for companies to automate intricate payment processes that have historically required a number of middlemen or manual reconciliation. For instance, when financial commitments are satisfied, supply-chain milestones are confirmed, or contractual criteria are met, funds may be delivered automatically. Instead of just transferring digital funds more quickly, MTN offers programmable features that have the potential to completely change the way institutional payments are made.

When taken as a whole, these programs show that Mastercard's blockchain strategy goes far beyond making cryptocurrency payments possible. The company is progressively building an integrated digital payments ecosystem that allows banks, businesses, merchants, and consumers to connect with regulated digital assets via well-known financial infrastructure. Stablecoins are now part of Mastercard's larger plan for contemporary financial services, rather than being viewed as a specialised form of payment.

From Consumer Payments to Core Settlement Infrastructure

Accurately determining its adoption stage is one of the most crucial components of Mastercard's most recent announcement. While the growth of stablecoin settlement is a significant development, it should not be confused with a full blockchain migration of Mastercard's worldwide settlement system.

Rather, the program is the result of a well-planned rollout that has developed over a number of years.

The initial stage was mostly concerned with customer access. Mastercard issued payment cards that enabled consumers to spend digital assets via its current merchant network in collaboration with cryptocurrency exchanges and wallet providers. Consumers were introduced to blockchain through these programs, which did not require merchants to implement new payment methods.

Merchant enablement was added to the second phase. Mastercard made it possible for merchants to obtain settlement in regulated stablecoins like USDC through partnerships with Circle and Nuvei. Around the same time, Mastercard Move started to enable stablecoin payouts, enabling banks to use blockchain technology to speed up cross-border transfers.

The third phase is institutional settlement infrastructure, which begins with the most recent announcement. Mastercard is incorporating regulated stablecoins into the settlement procedures that take place between issuers, acquirers, and payment processors rather than restricting blockchain to the periphery of the payment experience. Early adopters, such as ARQ, CBW Bank, Cross River Bank, Lead Bank, and Nuvei, are starting to apply these features in a few Latin American and American markets.

Crucially, rather than being a whole worldwide deployment, this should be categorised as a constrained production rollout. For a limited number of partners, the settlement capacity is operational; nevertheless, participation is still optional, regional growth will continue until 2026, and traditional fiat settlement will continue to be the default choice throughout the majority of Mastercard's network.

Mastercard's more general approach to institutional blockchain adoption is shown in this methodical approach. Instead of trying to replace its infrastructure on a wide scale, the corporation is implementing blockchain gradually, which results in quantifiable operational gains. Mastercard is able to increase adoption while preserving operational resilience and regulatory compliance because each step builds upon capabilities that have already shown practical usefulness.

Source: Mastercard

What This Means for the Payments Industry & the Broader Blockchain Ecosystem?

Mastercard's stablecoin approach is part of a larger trend in the way large financial institutions are using blockchain technology. Companies are increasingly embracing blockchain as an infrastructure that may enhance particular operating procedures rather than seeing it as a substitute financial system.

With regard to the payments sector, Mastercard's most recent project shows that blockchain is starting to extend beyond consumer-facing cryptocurrency products into domains where payment efficiency has historically relied on banking infrastructure. Despite notable advancements in digital payments, settlement, liquidity management, and treasury procedures have remained mostly unaltered for decades. By incorporating regulated stablecoins into these processes, settlement flexibility might be increased without forcing institutions to give up on their current payment networks.

This gives payment processors and banks new ways to handle liquidity. For organisations that operate in several countries, continuous settlement outside of regular banking hours could improve cash flow management and lower idle capital requirements.

Additionally, the effort offers blockchain infrastructure providers significant validation. Mastercard has embraced a multi-network strategy that incorporates Ethereum, Base, Arbitrum, Polygon, Solana, XRPL, and Canton rather than depending just on one blockchain. This indicates that a single blockchain is unlikely to dominate enterprise adoption. Depending on variables like throughput, transaction costs, compliance requirements, and ecosystem maturity, various networks may increasingly meet distinct institutional demands.

Mastercard's growing support for stablecoin issuers highlights the significance of regulated digital currencies in traditional finance. The stablecoins of Circle, Paxos, Ripple, and SoFi are progressively being included into the payment infrastructure utilised by banks, payment processors, and international retailers; they are no longer exclusively involved in crypto-native ecosystems.

Additionally, the program is in line with Mastercard's involvement in larger industry partnerships that aim to enhance financial institutions' interoperability. Instead of growing into separate blockchain ecosystems, the company is investigating how tokenised deposits, programmable payments, and regulated digital assets may coexist within a shared financial infrastructure through initiatives like the Multi-Token Network.

Challenges That Could Influence Mastercard's Stablecoin Strategy

Although Mastercard's approach is among the most thorough institutional deployments of stablecoins to date, a number of factors other than the technology itself will determine its long-term viability.

- Regulatory fragmentation: Different jurisdictions still have different laws governing stablecoins. Expanding settlement services internationally will necessitate adjusting to various legal and regulatory constraints, even while Mastercard supports regulated issuers and has reinforced its compliance structure through regulatory licenses like the New York BitLicense. In markets where regulatory clarity is still developing, this could impede deployment.

- Blockchain and legacy system interoperability: Mastercard's hybrid strategy relies on smooth connectivity between various blockchain networks and conventional banking infrastructure. Although supporting Ethereum, Polygon, Solana, Base, XRPL, and Canton adds integration complexity and necessitates uniform standards for settlement, compliance, and reconciliation, it also offers flexibility.

- Scalability at enterprise volumes: Every year, Mastercard handles billions of transactions. Supported blockchain networks must show that they can sustain predictable transaction costs, dependability, and performance under enterprise-scale demand without sacrificing user experience as stablecoin settlement grows.

- Institutional preparedness and operational transformation: Before implementing stablecoin settlement on a large scale, financial institutions must update their internal systems, risk management procedures, and treasury procedures. Even though the technology is currently available, its widespread adoption will ultimately depend on whether businesses observe quantifiable increases in liquidity, operational effectiveness, and settlement speed.

- Sustaining confidence in regulated stablecoins: The Mastercard ecosystem depends on regulated stablecoins issued by companies like SoFi, Paxos, Ripple, and Circle. Maintaining institutional trust and promoting greater involvement will need ongoing disclosure regarding reserves, governance, and regulatory supervision.

By maintaining traditional fiat settlement alongside blockchain-based alternatives, Mastercard reduces migration risk while allowing institutions to adopt stablecoins gradually as business needs evolve.

A Pragmatic Path Forward

The most recent stablecoin project from Mastercard is the result of a larger plan that has gradually incorporated blockchain into consumer payments, merchant settlements, international transfers, and now institutional settlements. The company is expanding its current infrastructure with regulated, blockchain-based settlement options to increase flexibility and operational efficiency instead of replacing conventional payment rails. Building on years of gradual development, the effort demonstrates true institutional blockchain adoption, even though it is still in a limited deployment. Mastercard's strategy may serve as a useful model for how conventional financial institutions integrate blockchain technology into regular payment infrastructure as regulatory frameworks develop and participation grows.

If you find any issues in this article or notice missing information, please feel free to reach out at team@etherworld.co for clarifications or updates.

To promote your Web3 articles, events, and projects, you may reach out anytime via EtherWorld PR for submissions and collaboration.

Related Articles

- Ecosystem Spotlight: The Graph, Ethereum’s Data Layer

- Who's Building for Ethereum's AI Agents?

- Proving Ethereum: 9 ZK Projects to Watch in 2026

- Where RWAs Go Next: 6 Projects to Watch

- Best Crypto DEXes Every DeFi Trader Should Know

To follow blockchain news, track Ethereum protocol progress, and read our latest stories, subscribe to our weekly today.

Join the EtherWorld & Avarch Internship Program and build your career in blockchain, content, social media, video, podcast editing, or operations. Send your resume and brief introduction to contact@etherworld.co.

Disclaimer: The information contained in this website is for general informational purposes only. The content provided on this website, including articles, blog posts, opinions, & analysis related to blockchain technology & cryptocurrencies, is not intended as financial or investment advice. The website & its content should not be relied upon for making financial decisions. Read full disclaimer & privacy policy.

To stay updated on blockchain news, Ethereum protocol progress, and our latest stories, subscribe to our weekly digest and YouTube channel for ELI5 content.

To promote your Web3 articles, events, project updates, and Press Releases, reach out anytime via EtherWorld PR for submissions and collaboration. For other queries, email contact@etherworld.co.

If you’d like to support our work, share the content and consider donating at avarch.eth.

Join our community on Discord and follow us on Twitter, Facebook, LinkedIn & Instagram.

Author

Nidhi Kumari is a Web3 content writer at EtherWorld.co, tracking ecosystem developments, funding activity, and market trends shaping the crypto space.