Where RWAs Go Next: 6 Projects to Watch

From Ondo and Securitize to Chainlink and Maple, these six projects are shaping the next phase of real-world asset tokenisation by tackling liquidity, compliance, distribution, and interoperability.

The first wave of real-world asset (RWA) tokenisation significantly addressed a technical question regarding whether traditional assets could be represented and transacted on blockchain networks. An increasing number of people are responding "yes." The more crucial question now is whether tokenised assets can become investable, composable, and globally distributed financial goods.

That issue is still unresolved. With stablecoins excluded, the market for tokenised RWAs has grown to over $24 billion, although usage is still highly concentrated. Private credit continues to be the most productive collateral used in DeFi, U.S. Treasury goods are the most commonly issued, and secondary liquidity is still limited in a number of asset types. Putting securities on the chain is no longer enough.

Today's most popular initiatives aren't always those that are issuing the most tokenised assets. Rather, they are tackling the structural hurdles that still prevent adoption, i.e., interoperability, distribution, institutional financing, regulatory compliance, liquidity creation, and specialised execution environments.

Together, the 6 initiatives listed below oversee about $15 billion in tokenised assets and enable billions of dollars in monthly transfers. More significantly, each is trying to address a unique issue that tokenisation by itself has not yet been able to resolve.

- Why RWAs Are Becoming Crypto's Most Valuable Market?

- 1. Ondo Finance

- 2. Securitize

- 3. Centrifuge

- 4. Plume

- 5. Chainlink

- 6. Maple Finance

- The Race to Build Useful RWAs

Why RWAs Are Becoming Crypto's Most Valuable Market?

Unlike previous bitcoin narratives that mostly depended on user growth or speculative demand, real-world assets are bringing current financial products, cash flows, and investors on-chain. Aside from stablecoins, tokenized real-world assets will have a market value of more than $24 billion by June 2026.

The business has expanded drastically over the last two years. Treasury-backed goods account for about half of this market, and private credit makes up a significant share, suggesting that investors favor yield-generating assets over purely speculative ones.

The inefficiencies that have afflicted traditional financial markets for decades can be resolved by RWAs, which makes them appealing. Conventional securities sometimes settle on a T+1 or T+2 basis, entail multiple intermediaries, and are not accessible to overseas investors due to jurisdictional restrictions and high minimum investment requirements. By reducing these processes to programmable smart contracts, tokenization enables fractional ownership, almost instantaneous settlement, and 24/7 accessibility.

Through institutional participation, their significance is becoming more apparent. Tokenized investment products have already been introduced by companies like BlackRock, Franklin Templeton, Apollo, and Janus Henderson, while platforms like Securitize are currently in charge of over $4.2 billion in distributed assets. With over 154,000 holders and a monthly transfer volume of over $3.6 billion, Ondo has demonstrated that demand is no longer limited to institutional investors.

But issuance is just one aspect of the problem. The majority of tokenized assets continue to struggle with interoperability, fragmented liquidity, and low secondary market activity. Because of this, the next stage of expansion is probably going to rely more on finding solutions for distribution, compliance, collateral utility, and cross-chain connectivity than on developing new tokenized products.

Projects like Ondo, Securitize, Centrifuge, Plume, Maple, and Chainlink are among the most keenly followed participants in the developing RWA ecosystem because they are trying to solve these exact issues.

1. Ondo Finance

Tokenised securities' largest problem is distribution rather than issuance. Tokenised funds have already shown interest from institutions, although the majority of products are still unavailable to international investors and are mainly isolated from crypto-native ecosystems.

In an effort to close that gap, Ondo Finance has become a formidable competitor.

As of June 23, 2026, Ondo supports 440 tokenised assets, has 154,602 holders, and permits a monthly transfer volume of about $3.62 billion. It is presently one of the biggest tokenisation platforms on the market, with a distributed asset value of $3.75 billion.

With a stated value of around $2 billion, Ethereum is still Ondo's largest deployment network. However, the protocol has spread to Stellar, Solana, BNB Chain, XRP Ledger, Sei, Mantle, Sui, Noble, and Aptos.

Ondo stands out because it is constructed to create demand rather than just increasing the supply of assets.

Blockchain-native access to short-duration U.S. Treasuries is made possible by products like USDY and OUSG, but Ondo's larger goal is to establish an ecosystem in which tokenised securities may be exchanged, traded, and eventually incorporated into decentralised apps similar to stablecoins.

The company views tokenised securities as a new asset category requiring specialised settlement infrastructure, as seen by the launch of Ondo Global Markets and its ambitions for Ondo Chain.

Few projects have successfully combined retail accessibility with institutional-grade assets on a large scale. The increasing number of Ondo holders indicates that there might already be a market for these goods.

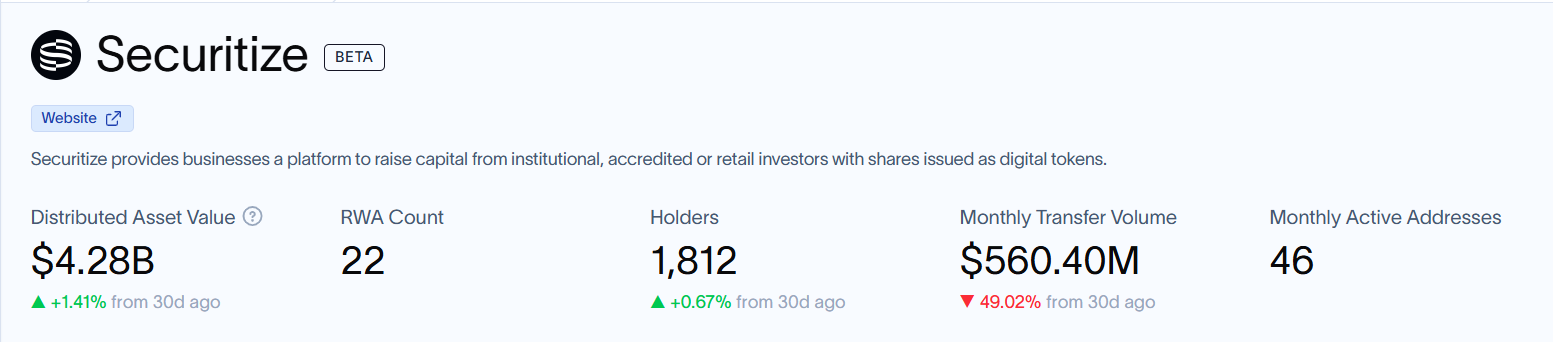

2. Securitize

If Ondo concentrates on distribution, Securitize has established itself as the institutional issuance operating system.

Although tokenisation is frequently addressed as a technological issue, traditional asset managers still place a significantly higher priority on administration and compliance. Issuers require KYC processes, cap table management, investor onboarding, transfer agent services, and regulatory reporting capabilities.

Building that infrastructure has taken years for Securitize.

Securitize presently manages $4.29 billion in distributed asset value, making it the largest platform among the programs looked at here. With 22 tokenised RWAs, over 1,800 holders, and monthly transfer volumes close to $572 million, its ecosystem is extensive.

The protocol has expanded beyond Ethereum as well.

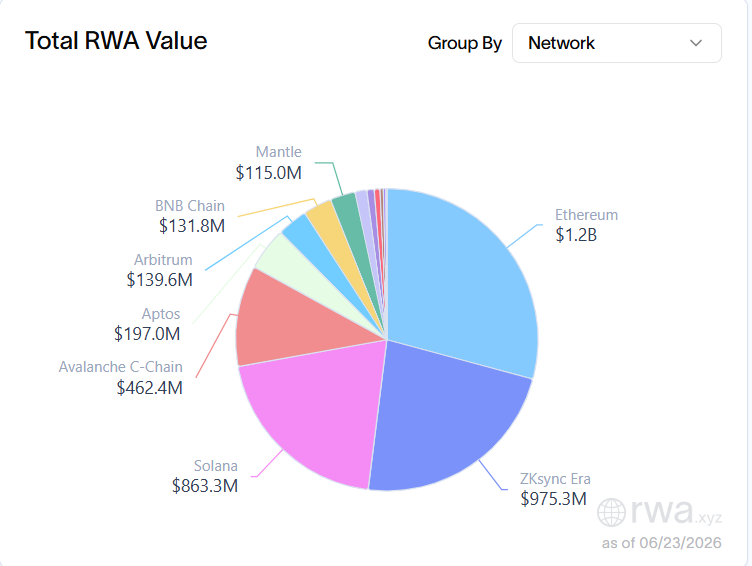

Securitized assets on Ethereum total almost $1.2 billion, while ZKsync Era has nearly $976 million. Another $863 million is contributed by Solana, indicating that multi-chain distribution schemes are becoming more and more popular among institutions.

After Securitize participated in BlackRock's BUIDL fund, its significance became increasingly clear.

Securitize serves as an enabler, enabling asset managers to tokenise funds without having to build blockchain expertise internally, as opposed to competing with established financial institutions.

Protocols that are only concerned with asset issuance could not be as durable as that position.

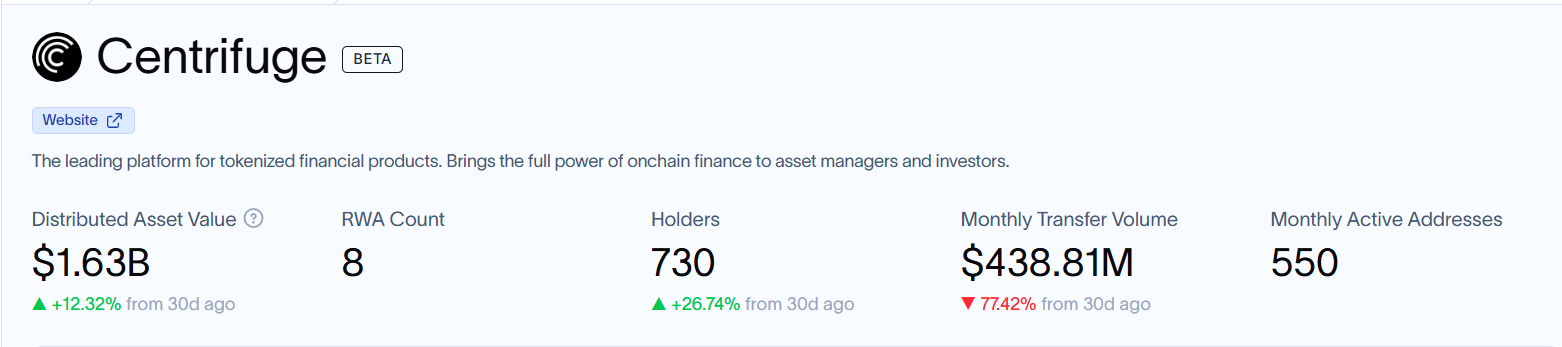

3. Centrifuge

Private credit remains one of the few RWA sectors that produce significant on-chain utility, despite Treasury products dominating headlines.

The projected value of the worldwide private credit market is approximately $1.7 trillion, and blockchain technology presents an opportunity to increase access to these historically illiquid instruments and enhance transparency.

Centrifuge has developed the most profound expertise in this area among RWA procedures. Centrifuge reported $1.63 billion in distributed assets as of June 2026, which is more than 12% greater than the month before.

Its network handles about $438.8 million in transfers each month, supports eight tokenised products, and has about 730 holders.

With $1.1 billion in assets, Ethereum continues to be the leading deployment network, while Avalanche, Solana, Base, and Plume together own more than $550 million.

The focus on productive collateral is what distinguishes Centrifuge.

Instead of depending only on passive Treasury exposure, the protocol has fostered connections with institutional borrowers, asset originators, and fund managers.

Its cooperation with Janus Henderson, creation of the Anemoy Treasury Fund, and integration with MakerDAO show a readiness to cater to conventional credit markets rather than just cryptocurrency-native investors.

Centrifuge has a legitimate niche due to its specialisation.

The primary means of competition for the majority of tokenised Treasury instruments is yielding differentials expressed in basis points. Private credit products compete based on their capacity for portfolio development, borrower quality, and underwriting skill.

4. Plume

Numerous tokenisation projects continue to run on general-purpose blockchains intended for permissionless applications and censorship resistance.

Plume is adopting an alternative strategy.

It makes the case that specific infrastructure is needed for real-world assets, integrating tokenisation engines, identity systems, licensing frameworks, and compliance modules straight into the network architecture. Builders are drawn to that thesis.

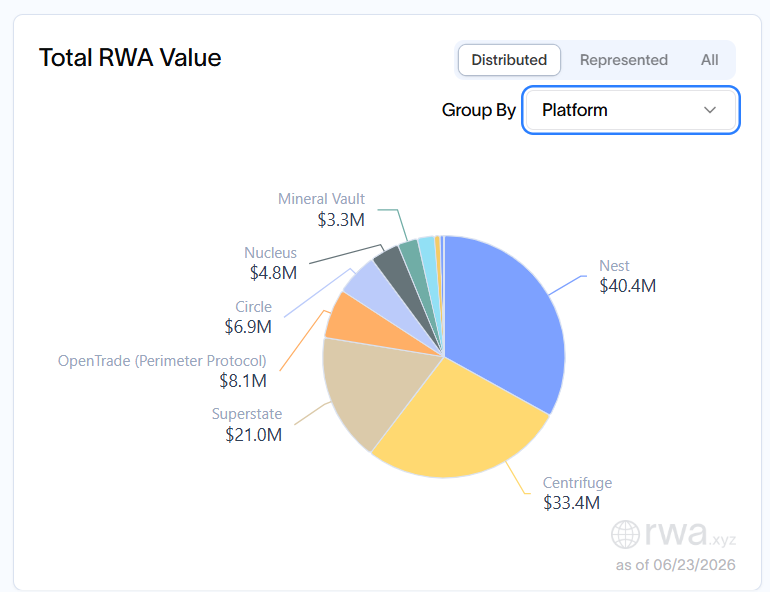

Plume presently serves about 249,295 holders, supports 210 RWAs, and records over $519 million in 30-day RWA transfer activity. Its represented asset value is $33.46 million, but its distributed asset value is over $109 million.

Activity growth is possibly the most noteworthy metric.

While RWA transfer volume jumped by around 947%, stablecoin transfer volume grew by more than 108% month over month.

According to platform-level data, Nest's value is approximately $40.4 million, followed by Centrifuge ($33.4 million), Superstate ($21 million), and OpenTrade ($8.1 million).

Although these numbers are still modest when compared to Ethereum-based ecosystems, they show that Plume is starting to draw a variety of issuers. Whether or not institutions favour purpose-built environments over modifying current public chains will determine their long-term success.

Plume is one of the more intriguing attempts in the RWA landscape because that topic is still open.

5. Chainlink

Blockchains alone are insufficient for tokenised assets.

They also require synchronised net asset value updates, cross-chain messaging, evidence of reserves, and precise pricing information.

Chainlink has progressively established itself as the infrastructure supplier in charge of these tasks.

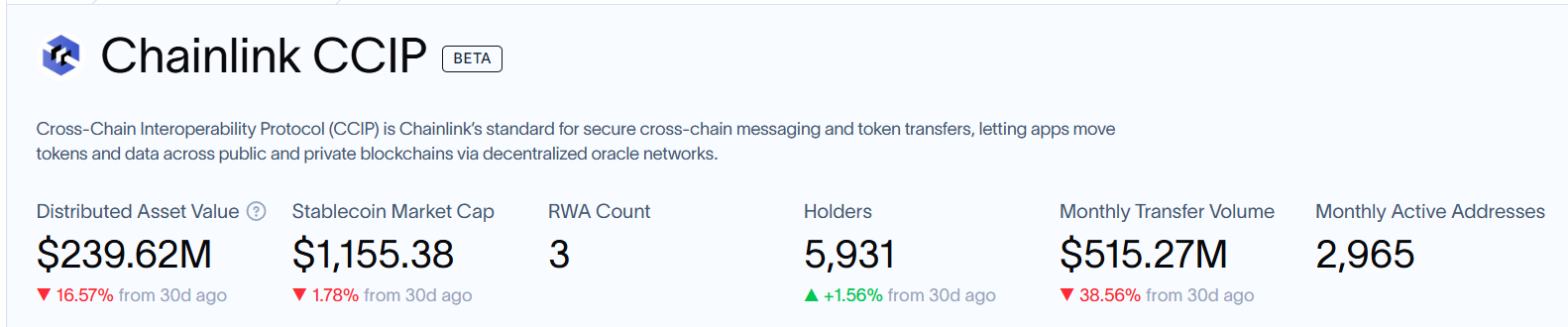

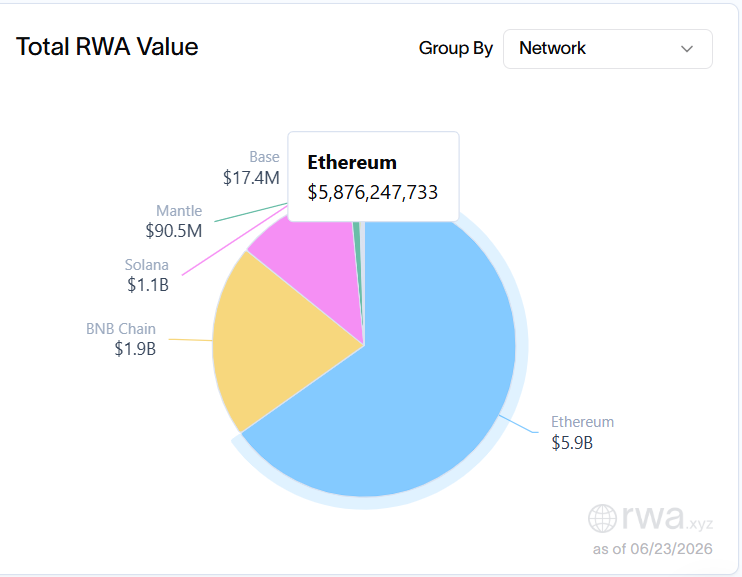

Chainlink's CCIP ecosystem has amassed almost 5,931 holders, supports three tokenised RWAs, and secures about $239.6 million in dispersed assets. Currently, more than $515 million is sent each month.

With a represented value of $5.9 billion and a market share of over 65%, Ethereum leads the network, followed by BNB Chain at $1.9 billion and Solana at $1.1 billion.

The significance of the protocol goes beyond these numbers.

In order to increase collateral mobility, DTCC has finished trial programs using Chainlink standards. Tokenised securities have operational difficulties in the absence of middleware suppliers.

The net asset values of funds may become obsolete. Distributions of coupons might be delayed. Settlement risks arise from cross-chain transfers.

During trading hours, traditional ETFs consistently release indicative NAV computations. The goal of Chainlink is to offer the blockchain version of that infrastructure.

This function might become essential when tokenised assets spread among several chains.

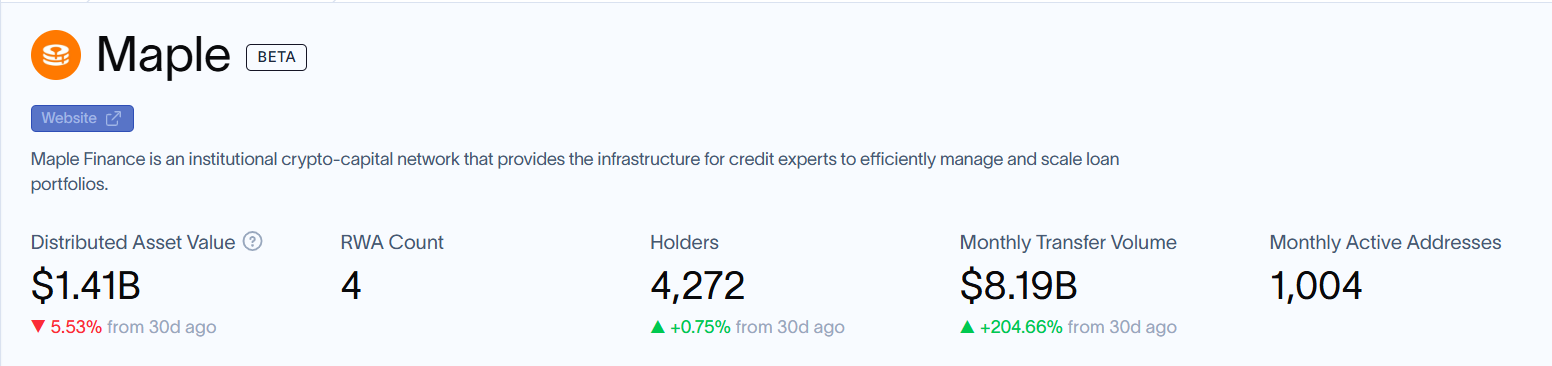

6. Maple Finance

The thesis of Maple Finance is distinct.

Maple focuses on institutional lending rather than Treasury bonds or issuance infrastructure. After a number of cryptocurrency credit platforms failed in 2022, a lot of investors wondered if unsecured lending would be able to return to blockchain markets.

Maple has gradually regained self-assurance.

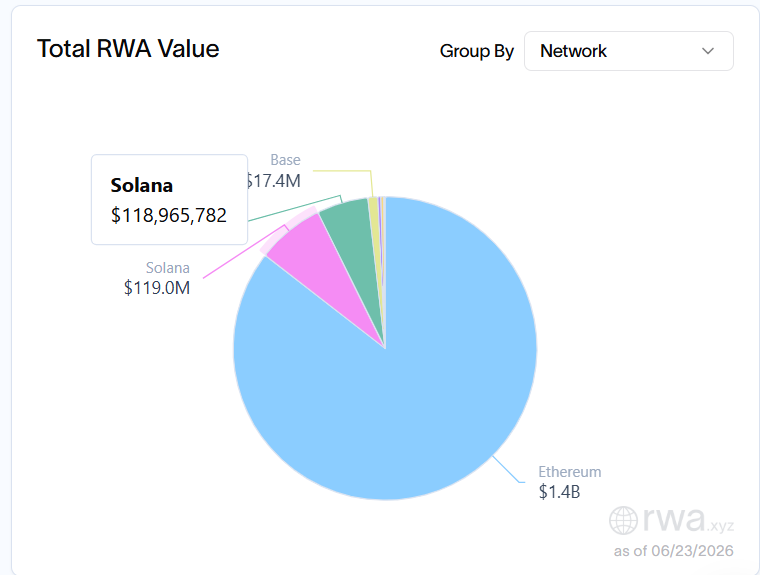

Approximately $1.42 billion in distributed assets are currently managed by Maple, with 4,270 holders taking part in its ecosystem.

The largest monthly transfer volume among the projects included in this article is more than $8.15 billion. About $1.4 billion of Maple's assets are housed on Ethereum, with $119 million coming from Solana and $90.5 million from Mantle.

In contrast to many RWA projects, Maple is not attempting to tokenise current financial products.

Rather, it offers the infrastructure necessary for credit professionals to create, oversee, and expand loan portfolios.

This distinction is important. The sector will eventually need active credit markets instead of just digital government bonds if tokenisation is successful.

Maple seems to be in a good position for that change.

The Race to Build Useful RWAs

Tokenisation is moving into a more challenging phase of its evolution. Proof that securities may be represented on blockchains is no longer needed by the industry. Evidence that tokenised assets may effectively circulate, draw users, connect with decentralised apps, and compete with conventional financial goods based on usefulness rather than novelty is required.

The aforementioned projects are working on various approaches to the problem.

Ondo is exploring with tokenized securities' worldwide dissemination. Institutions looking for infrastructure that is ready for compliance now favour Securitize as their issuing partner. Centrifuge keeps proving that, in terms of on-chain finance, private credit can still be the most productive category. While Chainlink is developing the middleware required to maintain tokenised markets synced across networks, Plume is testing whether RWAs need their own execution environment. According to Maple, one of the most resilient financial use cases for blockchain technology may be institutional lending.

The precise frictions they seek to remove, rather than the quantity of assets they tokenise, are what give them collective relevance. As the RWA market develops, those that enable tokenised assets to operate as smoothly as their conventional equivalents may emerge victorious rather than those who issue the greatest number of securities. As tokenisation advances from issuance to full-scale financial integration, these six initiatives are therefore among the most interesting to keep an eye on.

If you find any issues in this article or notice missing information, please feel free to reach out at team@etherworld.co for clarifications or updates.

To promote your Web3 articles, events, and projects, you may reach out anytime via EtherWorld PR for submissions and collaboration.

Related Articles

- Morpho Raises $175M in Largest DeFi Funding Round

- Europe Delists USDT as MiCA Rules Take Effect

- Hsiao-Wei Wang Steps Down From Ethereum Foundation Leadership

- Mastercard Launches Agent Pay for Machines to Power AI-Driven Commerce

- UNDP Brings 26 Blockchain Leaders Under One Roof

To follow blockchain news, track Ethereum protocol progress, and read our latest stories, subscribe to our weekly today.

Disclaimer: The information contained in this website is for general informational purposes only. The content provided on this website, including articles, blog posts, opinions, & analysis related to blockchain technology & cryptocurrencies, is not intended as financial or investment advice. The website & its content should not be relied upon for making financial decisions. Read full disclaimer & privacy policy.

To stay updated on blockchain news, Ethereum protocol progress, and our latest stories, subscribe to our weekly digest and YouTube channel for ELI5 content.

To promote your Web3 articles, events, project updates, and Press Releases, reach out anytime via EtherWorld PR for submissions and collaboration. For other queries, email contact@etherworld.co.

If you’d like to support our work, share the content and consider donating at avarch.eth.

Join our community on Discord and follow us on Twitter, Facebook, LinkedIn & Instagram.

Author

Nidhi Kumari is a Web3 content writer at EtherWorld.co, tracking ecosystem developments, funding activity, and market trends shaping the crypto space.